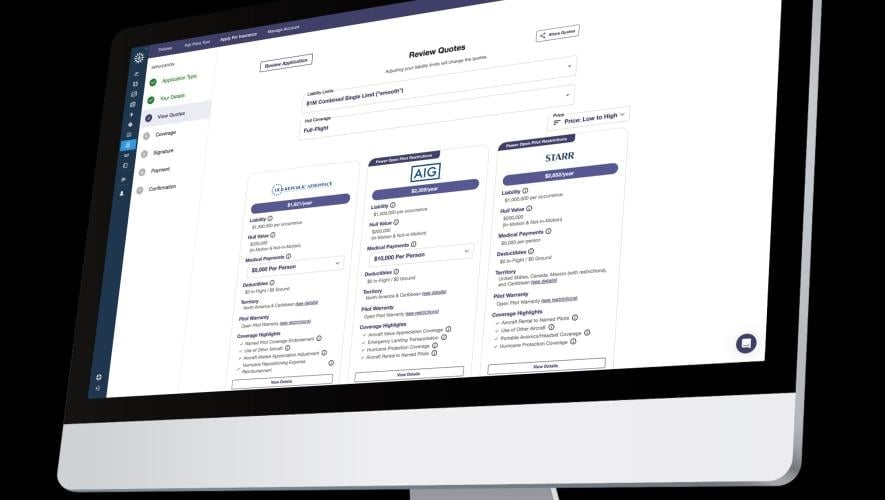

AINsight: Limiting Risk as Liability Insurance Tightens

In the last two years, many underwriters have exited aviation insurance while those remaining have tightened underwriting standards and hiked premiums.

David G. Mayer

AIN Contributor

About the author

David G. Mayer is a member of the global Aviation Practice Group at Shackelford, McKinley & Norton in Dallas, which handles private aircraft matters, including regulatory compliance, tax planning, purchases, sales, leasing and financing, risk management, insurance, aircraft management and operations, hangar leasing, and related corporate work. Mayer frequently represents corporations and high- and ultra-high-net worth individuals and other aircraft owners, flight departments, lessees, borrowers, operators, sellers, purchasers, corporations and managers, as well as lessors and lenders. He can be contacted at [email protected].