Closing in

0

...

Menu

Search

LATEST

POPULAR

AIRCRAFT FOR SALE

SECTIONS

Business Aviation

Defense

Aerospace & Air Transport

FutureFlight

Rotorcraft

General Aviation

SUSTAINABILITY & ENVIRONMENT

CHANNELS

Aircraft

Maintenance

Avionics

Charter & Fractional

Safety

All Categories

News Archive

Newsletter Archive

MORE

AIN FBO Survey

Airshows & Conventions

Aviation Events

Compliance Countdown

Expert Opinion

In-Depth Reports

Leeham News & Analysis

Print Archives

Videos

Webinars

Whitepapers

ABOUT

About AIN

Our Writers

History

Advertise

Contact Us

Subscribe

LATEST

POPULAR

AIRCRAFT FOR SALE

SECTIONS

ABOUT

Search

Subscribe

Search

Finance, Taxes, Insurance

Helicopter Insurance Premiums Could Double

Sticker shock looms for those renewing helicopter insurance policies.

Share

Post

Share

Print

Copy

Email

By

Mark Huber

• Contributor

December 17, 2018

More In Finance, Taxes, Insurance

U.S. Aerospace Chases Supply-chain Stability

AIA chief warns budget swings still threaten suppliers

Finance, Taxes, Insurance

Wheels Up Fleet Transition Completed Early by 5x5

Transition involved nearly 100 aircraft since early 2024

Finance, Taxes, Insurance

ForeFlight Adds Aircraft Owners to Insurance Offering

To be available starting at EAA AirVenture Oshkosh from July 20 to 26

Finance, Taxes, Insurance

Rocket Lab To Acquire Iridium Communications in $8B Deal

Deal is expected to close in mid-2027

Finance, Taxes, Insurance

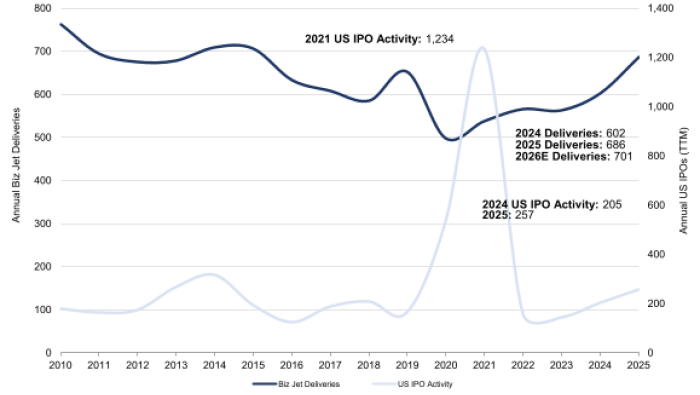

Record IPO Activity Signals Strong Bizjet Outlook

Capital markets activity historically tracks bizjet delivery trends

Finance, Taxes, Insurance

Honeywell Aerospace Cleared for June 29 Stock Spinoff

Honeywell board approved aerospace unit’s separate Nasdaq listing

Finance, Taxes, Insurance

Hybrid-electric Aircraft Developer Maeve Goes Bankrupt

Dutch start-up failed to raise the €20 million it needed to continue

Finance, Taxes, Insurance

China's Volant Aerotech Secures Additional eVTOL Funding

New Series C investment to support 2027 certification goal

Finance, Taxes, Insurance